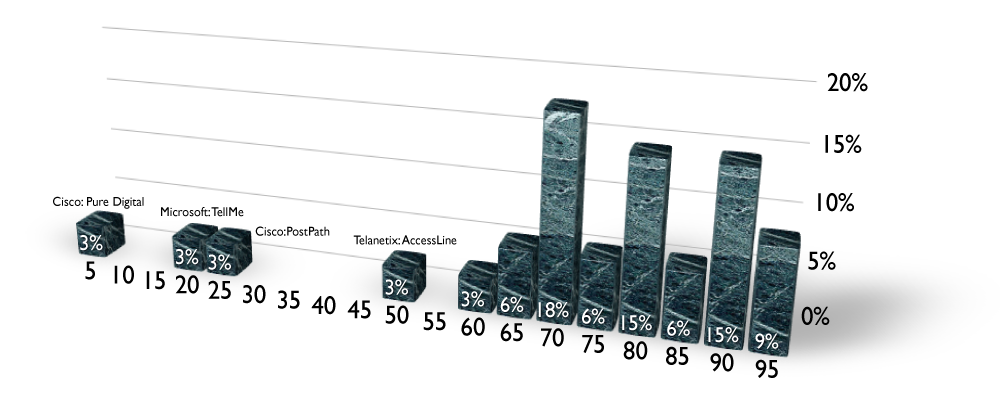

Aastra Technologies of Concord Canada has become an astute product line acquisitor. Back in the telecom boom days, Aastra bought the telephone product line from Nortel, secured a supply agreement to deliver telephones and IP phones to Nortel and propelled that unit into the SIP phone business. Also, in 2001 Aastra picked up the dense remote access concentrator product CVX-1800 from Nortel (designed by Aptis and acquired in 1998 by Nortel).

In 2004, Aastra acquired the EADS enterprise telephony business in a transaction priced at €72.5 million, which at the time employed about 730 employees roughly half in western Europe and the rest in the US.

And on February 18, 2008 Aastra announced the acquisition of Ericsson's enterprise communications business for $130 million. The unit has 630 employees in 30 countries and generated $460 million in revenues in calendar 2007.

Brockmann rating on this deal is as follows:

Strategic fit [5/5].

Aastra has chosen to concentrate on established PBX product lines that complement their developing competencies in IP phones and applications. As well, the Ericsson Enterprise had several mobile-enterprise innovations in their portfolio and the Intecom unit will appreciate access to this technology for their installed base. Both the Ericsson and Intecom units can and are likely to leverage each others' competencies and technologies. Aastra is picking up enterprise telephony units with specific market strengths (regional strength in the case of Ericsson and very large enterprises for Intecom).

Timing [5/5].

February 2008 was a great time to announce. Far enough before VoiceCon to communicate directly to customers and still well ahead of any deal for Siemens Enterprise, this deal and this business is 'chewable' for Aastra. Siemens is a $5 billion business, while Ericsson's is 10% of that and although is likely to be a strong contributor to Aastra profits (no mention of their earnings contribution on any press releases…), there could be financial surprises that could easily chew up Aastra's bottom line ($17 million/quarter in 4Q07).

Customer demand [2/5].

Ericsson's customers, like the other Aastra customers are market laggards. They are very conservative when it comes to communications brands and technologies. That means they don't count on innovative features or jump on technology bandwagons the first year they're out. Frankly, I suspect that Ericsson's customers are happy that the product line (MD-110) won't be discontinued anytime soon.

Potential [4/5].

A well run PBX business ought to generate in the range of 5-10% profit. So, this transaction could easily double Aastra's earnings, as it will also greatly increase its revenues propelling them past the hallowed $1 billion revenue range.

Overall: 16/20 = 80%.